If someone had given me a crystal ball a year ago and asked me to hypothesize in the next twelve months, the word “pandemic” would not have been at the top of my list. Trade wars (read China), the US presidential election, Brexit, economic outlook, climate change – all of these would have made the top ten.

Pandemic? Lockdowns? Furlough? I’ll leave that to Hollywood. Twelve months on, and perceptions have changed, brought on by an invisible virus, whose ability to spread seems to know no bounds. Going shopping? – wear a mask; take your children to school? – hand sanitizes; don’t stand closer than six feet to someone, not in your social bubble. Just when the BVI was moving away from the shadow of Irma, a new, but more sinister, natural phenomenon was taking over our existence.

The question we all want to know – when will it end?

General Impact of the Pandemic.

With the mention of a new flu-like virus circulating in Wuhan City, China at the start of 2020, little attention was paid by the West to the first reports, probably a reflection of how SARS and then MERS both petered out in earlier years without spreading too far – certainly not enough to worry about from our Western sanctuary. By early February, Western countries were paying attention to the first cases being detected (although later research demonstrated that the virus had spread out of China before the end of 2019), and by the end of March, much of the world was in lockdown.

Different strategies for coping with the spread of the virus, contributed to the rapid transmission amongst the population, with countries slow to ban flights from impacted areas and to undertake community testing once test kits were available. Now, some eight months later, countries are struggling to keep their economies open, as the second wave of the pandemic surges through America and Europe with politicians balancing the need to encourage people back to work and keep schools open, against the rise of transmissions within the local population and overwhelming health systems. There are no easy choices.

The Caribbean region, and other island nations, have generally been an example of how to isolate, with Governments quick to close borders and issue strict lockdown measures in an attempt to prevent the spread of the virus. However, when some island economies opened up in July, there was a spike in cases from visitors and returning nationals as seen in the Bahamas, Turks and Caicos Islands, and Barbados, demonstrating just how difficult it can be to re-open borders and keep the virus at bay.

Apart from a single spike from returning nationals in late June, Antigua has so far managed both to open the island to tourism and manage cases very well, keeping infections low. Graph 1 shows the number of infections per day for the Turks and Caicos Islands and Antigua & Barbuda, indicating the impact of reopening borders on different islands. For most of the summer months of 2020, the BVI coped incredibly well with just eight confirmed cases (and sadly one death) and a healthy internal economy, before a border breach from the US Virgin Islands introduced the virus into the general population. As shown in Graph 2, cases spiked within two weeks and the BVI went back into curfew at the end of August. Thankfully, by late September, this flurry of cases appeared to be under control and the Government announced plans to open the borders to tourists from 1 December initially much to the relief of local businesses and potential tourists alike.

After the initial announcement that the BVI would open to tourists on 1 December, the Government held consultations with local stakeholders to obtain feedback on their provisional protocols. Despite concerns within the tourism and business community that the protocols would create an unattractive framework for visitors to enter the BVI, they were announced by the Government on 26 October. The initial reaction was not positive from either the business community or the many tourists who had been holding reservations, and in the first few days after the announcement, many reservations were canceled.

The protocols, as announced on 26 October, required hotels and villas to be certified as approved establishments, with staff trained in dealing and working with COVID-19. Tourists, needed to undertake a total of four PCR tests (before arrival, on-arrival, day four, and day 8) as well as quarantine in the approved establishment for eight days. If the tourist had a negative test on day four, they were to be allowed some additional limited access to unspecified locations within the BVI. A negative test on day 8 would have allowed open access to the BVI.

This has all been updated, with quarantine days now standing at four. As we enter 2021, the government has begun the rollout of the vaccine, with the UK having dispatched a total of 8,000 doses, with more forthcoming by the end of the first quarter. Notwithstanding the vaccine rollout, governments still need to plan for another twelve months of disruption, providing support to businesses struggling to cope with the extended impacts of the pandemic. In the BVI, there are serious concerns in the tourism sector as to how companies will survive without a viable high season. Initial reactions from tourists to what seemed onerous protocols were not encouraging and it is now clear that there will not be a season per se. The impact on the world economy, resulting from the pandemic has been wide-ranging, with Governments putting emergency measures in place to protect people and businesses, resulting in a substantial increase in national debt. To put this in context, the Centre for Strategic and International Studies estimated that around US$7 trillion of debt had been incurred by the G20 countries on direct spending, tax relief, and lending by the end of May 2020, which far exceeded the fiscal support given by Governments during the economic downturn of 2008-10.

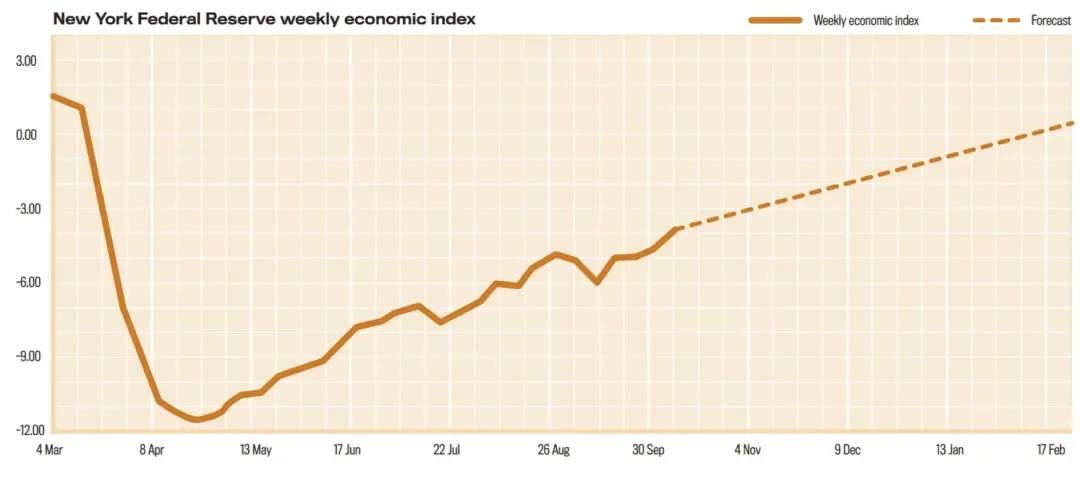

The need for Government support continues as the impacts of the pandemic show no sign of slowing, and predictions for economies to rebound in the near term are now being questioned as Governments are tackling the second wave of the pandemic and being forced into tiered lockdowns depending on regional severity. The role of central banks in the support of economies mirrors the actions taken following the 2007 financial crisis, with quantitative easing (QE) programs employed to enable central banks to purchase Government debt, to keep the cost of government borrowing low. In short, the QE approach helps stabilize economies and keeps interest rates down. The economic recovery in the US has been more promising as GDP reflected significant growth from the reopening of the economy over the summer and the New York Reserve’s Weekly Economic Indicator indicated the economy was -3.9% behind the same mid-October period a year prior as shown in Graph 3.

By the end of September, over half the jobs lost in March and April had been regained. The US housing market is performing strongly with increases in both new start development and re-sales, bolstered by the Federal Reserve stating that interest rates will not change until inflation increases.

This has all been updated, with quarantine days now standing at four. As we enter 2021, the government has begun the rollout of the vaccine, with the UK having dispatched a total of 8,000 doses, with more forthcoming by the end of the first quarter. Notwithstanding the vaccine rollout, governments still need to plan for another twelve months of disruption, providing support to businesses struggling to cope with the extended impacts of the pandemic. In the BVI, there are serious concerns in the tourism sector as to how companies will survive without a viable high season. Initial reactions from tourists to what seemed onerous protocols were not encouraging and it is now clear that there will not be a season per se. The impact on the world economy, resulting from the pandemic has been wide-ranging, with Governments putting emergency measures in place to protect people and businesses, resulting in a substantial increase in national debt. To put this in context, the Centre for Strategic and International Studies estimated that around US$7 trillion of debt had been incurred by the G20 countries on direct spending, tax relief, and lending by the end of May 2020, which far exceeded the fiscal support given by Governments during the economic downturn of 2008-10.

The need for Government support continues as the impacts of the pandemic show no sign of slowing, and predictions for economies to rebound in the near term are now being questioned as Governments are tackling the second wave of the pandemic and being forced into tiered lockdowns depending on regional severity. The role of central banks in the support of economies mirrors the actions taken following the 2007 financial crisis, with quantitative easing (QE) programs employed to enable central banks to purchase Government debt, to keep the cost of government borrowing low. In short, the QE approach helps stabilize economies and keeps interest rates down. The economic recovery in the US has been more promising as GDP reflected significant growth from the reopening of the economy over the summer and the New York Reserve’s Weekly Economic Indicator indicated the economy was -3.9% behind the same mid-October period a year prior as shown in Graph 3.

By the end of September, over half the jobs lost in March and April had been regained. The US housing market is performing strongly with increases in both new start development and re-sales, bolstered by the Federal Reserve stating that interest rates will not change until inflation increases.

However, once the Workers Stimulus Payment scheme ended in July, the partisan negotiations on the COVID-19 relief bill for continued financial support ended abruptly in early October with the then President terminating discussions with his Democratic rivals, until after the election leading to concerns that the economic recovery could stall as job losses accelerate.

Any new stimulus package now rests on the shoulders of the new administration with a $2 trillion stimulus package on the table. Any continued delay in negotiating the stimulus package risks the economy falling into recession. While the national lockdown has been devastating for many, particularly where jobs have been lost, the chance to work from home, cutting out travel costs and child care fees plus extraneous social expenditure, has led to a spike in savings which nearly quadrupled in the US between February and April 2020, peaking at 33.6% of income after taxes. This reflects the uncertainty that people feel about their immediate future and the need to pay off debt and build up savings, thereby limiting the expenditure that would otherwise help boost the economy.

When Government income support winds down, it will be the lower-income earners and unemployed who will be facing a bleaker future. The pandemic may also be fostering some long-term trends as high[1]speed internet connections have lessened the need to work in an office and enabled children to be schooled online. The growth of Amazon and online shopping has accelerated, as consumers have sought to avoid unnecessary social interactions, with retail outlets impacted through reduced market share. When the vaccine is eventually universally available, we will emerge into a different world where a single natural phenomenon will have altered the way we interact.

BVI Government’s response to the pandemic

The Government’s reaction in March of last year to the pandemic and a quick lockdown was widely praised as it effectively stopped the spread of the virus with the result that few cases emerged. However, these measures had a significant financial impact on the BVI, not just in terms of lost income through lower taxes (payroll tax, NHI, social security) as employees have been laid off but the corresponding increase in costs resulting from the support package the Government has put in place. Announced in early June, the BVI Government’s stimulus package comprised $62.9M, funded primarily by the Social Security Board through a $40M grant. This grant was divided into a $10M unemployment fund; $9M to repair homes damaged in the 2017 hurricanes; $6.5M in business grants; $7.5M to support the NHI program and allocations to support various industries including hospitality, daycare, fishing, and farming.District representatives and at-large representatives also had $300,000 to spend on a discretionary T BVI Government’s response to the pandemic basis. As part of the larger package, the Government revived a $17M Social Security Board housing project at Joe’s Hill providing 43 residential units for first-time owners and also committing a further $2M to infrastructure projects. The Government has yet to announce whether it will extend the “lay[1]off” period which expired on 31 October.

This is the time allowed by employers to temporarily lay-off employees without having to sever them which was extended in June from three months to seven months. This extension, combined with the Government’s unemployment fund, has been the main support for local business owners who have been unable to operate without the tourist industry or for other reasons. If the decision is made not to extend the lay-off period, then many firms may have to sever employees, which will make it much more difficult to restart the economy once the BVI does re-open. This is, due in large part to the time taken to process work permits for any positions which cannot be filled locally.

BVI & UK Relations

A shortfall of $42M in government revenues in 2020 is projected as a result of the pandemic, the BVI Government has petitioned the UK Government to make changes to the regulations and protocols for how the BVI borrows and spends money. First established in 2012, the Protocols for Effective Financial Management set out the limits for Government spending and borrowing, but are now seen by the BVI Government as being too restrictive at a time when the COVID-19 pandemic is reducing revenues and creating additional costs. While still to agree to any changes to the 2012 agreement, the UK has indicated, according to Premier Fahie, that there could be room for negotiation.The Government has a new agenda regarding the relationship with the UK and has set out the framework for discussions on the upcoming constitutional review. While the relationship between the BVI Government and the UK appointed Governor, has at times been strained since the 2019 elections, Premier Fahie has highlighted the need to update the 2007 constitution and address the UK/BVI relationship in light of the UK’s exit from the EU, the on-going recovery from the 2017 hurricanes and the continued contraction of the financial services sector. In late September, the move by the Governor to invite the Royal Navy to secure and patrol the BVI border against the stated wishes of the BVI Government created a diplomatic spat between the locally elected politicians and Whitehall. In June 2020, the Government announced the establishment of a Constitutional Review Committee which will conduct a full review of the 2007 constitution. The review will include public forums and should take approximately six months to conclude. Some areas the Premier wishes to see addressed, are the control of the public service through the Ministries rather than through the Governor, and the question of confidentiality in the interactions between the Governor and the Premier.

While discussions will address the nature of the relationship between the UK and the BVI, there have not been calls to seek A BVI and UK relations independence from the UK, at least publicly. One Minister has called for the relationship to move to a “free association”, whereby a relationship is maintained with the UK, but without controls over how the BVI governs itself. As the BVI approaches the 4 year anniversary of Hurricane Irma, the need to continue the recovery is as evident as before, with the Government announcing that it will encourage investment through infrastructure projects.

Post-Irma, the establishment of the Recovery and Development Agency (RDA) created an independent entity to administer the many expected contracts that would be awarded and managed in a transparent manner. While the RDA continues to approve, execute, and administer contracts under the BVI Recovery and Development Plan, the scope of the work undertaken by the RDA has been reigned in under the current administration which seeks to control what projects are approved and how the funds are administered. As part of the approval of the £300 million loan guarantee offered by UK as part of the recovery program, the current administration met with UK officials in September 2019 to discuss the terms and conditions for the guarantee. This resulted in a number of additional actions, including the preparation of the Recovery to Development Plan of the Virgin Islands 2019-2023 and the establishment of a Borrowing and Steering Committee, which will be the body responsible for securing loans under the UK’s guarantee including negotiating terms for any borrowing agreement within internationally adopted debt sustainability indicators.

The development plan was submitted to the UK Government for review and was approved by the BVI House of Assembly on 24 June 2020. The revised plan allows the BVI Government to renegotiate the terms and conditions offered by lending institutions such as the Caribbean Development Bank. The UK, as guarantor of the loan, has yet to approve the revised plan.

Distribution of Sales

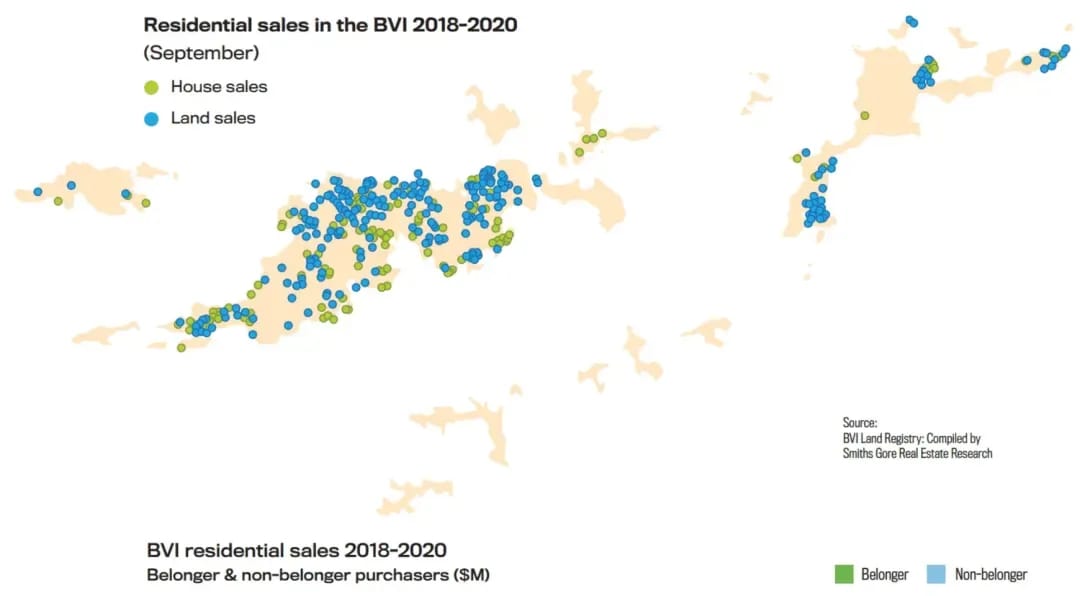

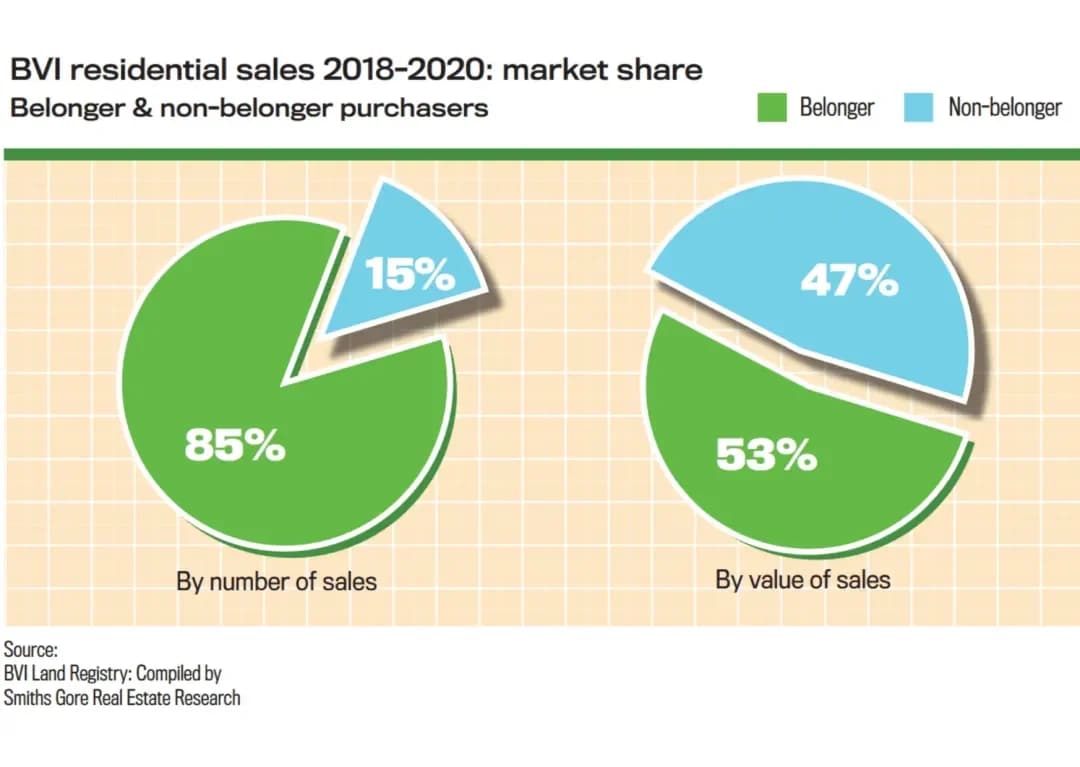

Map 1 identifies the distribution of sales of land and houses around the British Virgin Islands between 2018 and September 2020. While there is a predominance of land sales over this period, overall there has been a fairly even geographical spread of residential property sales in the BVI. Utilizing the same residential data set, we have also looked at how the sale of residential property has been divided between Belongers and Non[1]Belongers, with the data being presented in Chart 3. The distribution in total sale value is evenly spread with Belongers purchasing $88.5M in residential real estate over this time period in 452 transactions and Non-Belongers purchasing $79.3M in residential real estate in 78 transactions.

Map 2 illustrates the geographical spread of all residential property purchases in the BVI (land and homes) between Belongers and Non[1]Belongers from 2018 to September 2020. This map demonstrates the importance of resort locations for external investors with Belmont, Nanny Cay, Trunk Bay, Scrub Island, Little Dix Bay, Trunk Bay, Little Dix Bay, Moskito Island, Leverick Bay and Oil Nut Bay all featuring sales to Non-Belongers.

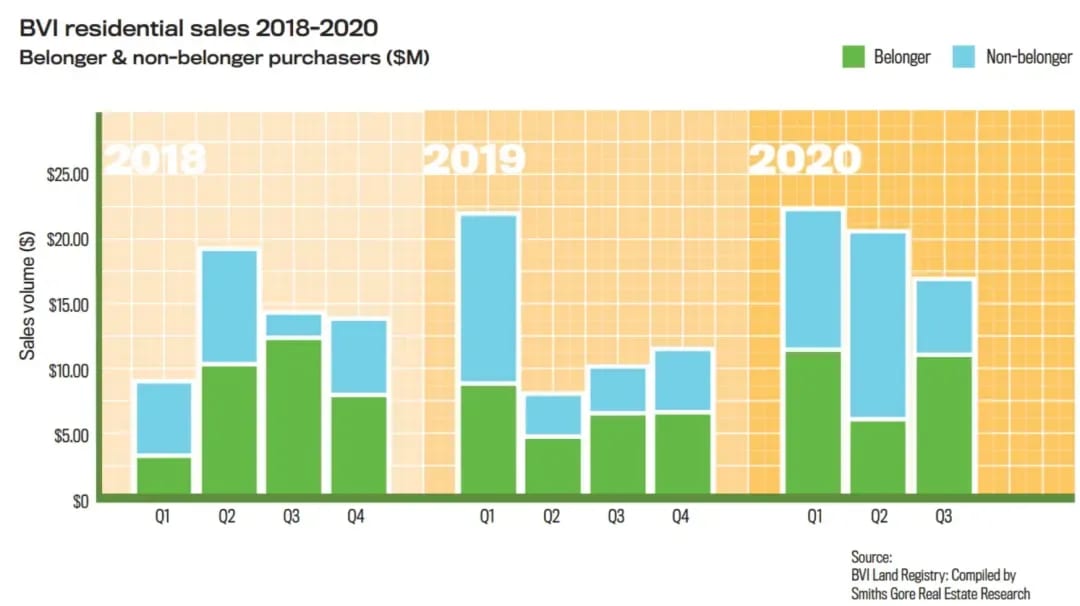

We do see a slight reduction in acquisitions by Belongers between 2018 and 2020, reflecting the initial flurry of activity amongst Belonger investors to acquire property in the aftermath of Hurricane Irma with Belongers purchasing $33.7M in residential real estate in 2018, reducing to $26.6M in 2019. There was an increase in residential property investment by Belongers in 2020 with a total spend of $28.3M by the end of September. In contrast, we see expenditure by Non-Belongers steadily increasing over this time period by 40%, reflecting the slow return to the market by external investors post Hurricane Irma. Sales to Non-Belonger investors totaled $22.57M in 2018, increasing to $25.2M in 2019. There was a total of $31.5M investment by Non-Belongers in residential real estate to September 2020.

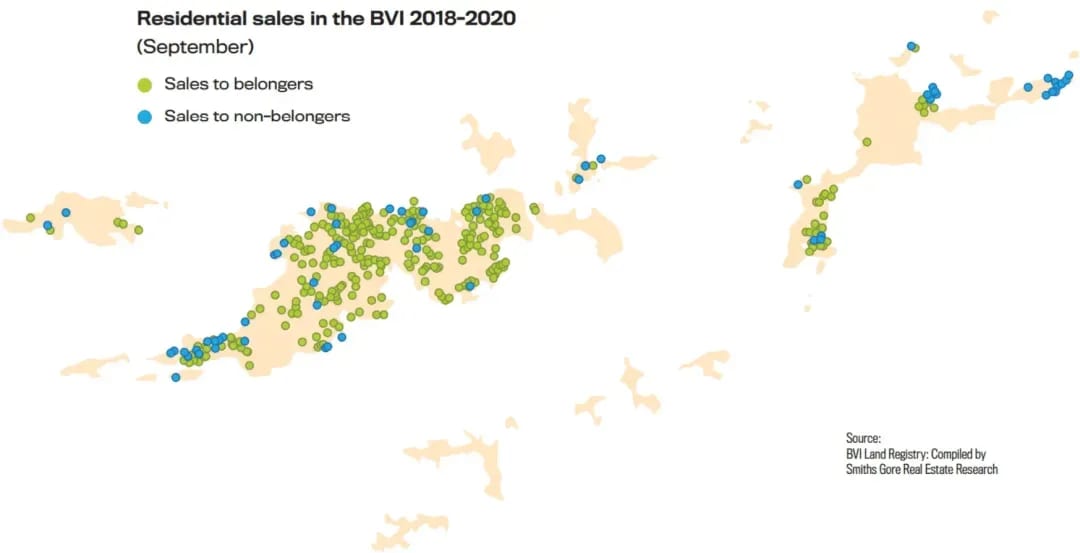

The overall impact of the map, however, is to demonstrate how Belonger investors in residential property have dominated the real estate market in the post-Hurricane Irma era. The acquisition of property is fairly evenly spread throughout Tortola although in Virgin Gorda there is a concentration of sales in The Valley and some sales in sub-divisions above Gun Creek/Leverick Bay overlooking North Sound. While the increase in investment by Belongers in the real estate market since Hurricane Irma is a welcome trend that returns land in the BVI to local ownership, the importance of external investment to the real estate market, and the finances of the BVI through stamp duty revenues, cannot be underestimated.

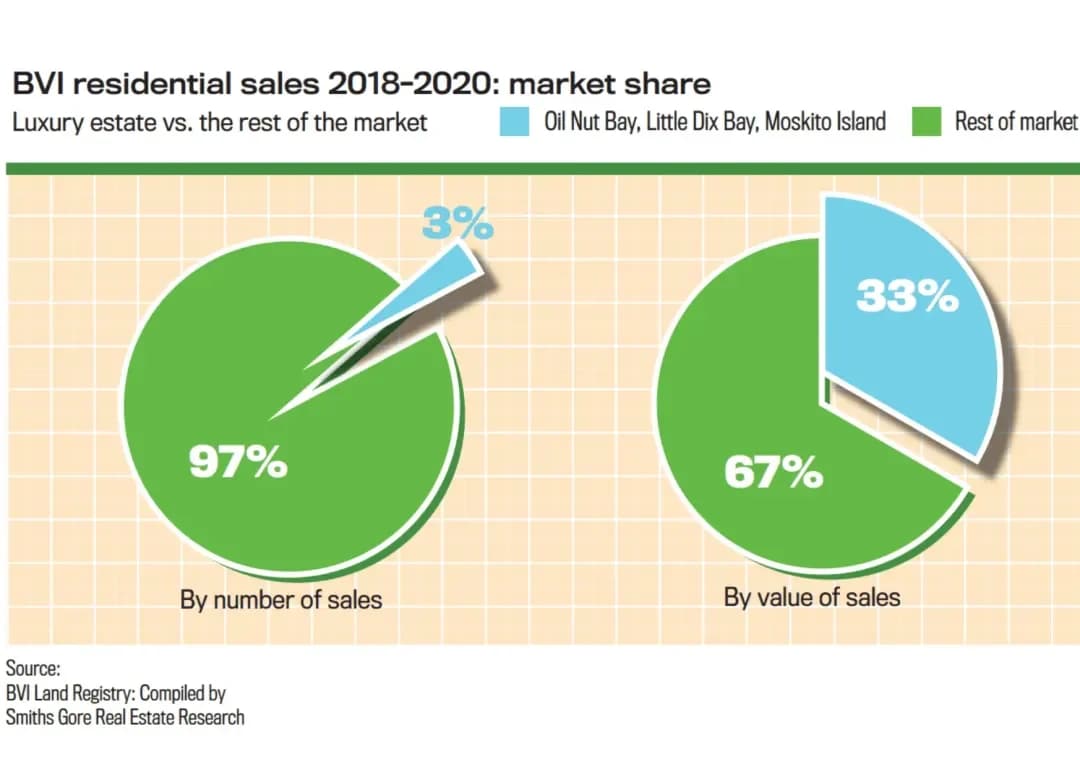

Chart 4 shows that while sales of residential property to Belongers accounted for 85% of all real estate transactions between 2018 and September 2020, these sales account for only 47% of the total value. This primarily reflects the activity of Belongers in the land market, where they account for 92% of all land sales compared to Non[1]Belongers who are predominantly active in the villa market. Total sales values ($M) from property sales in the BVI have been driven disproportionately by sales on the major resort and residential developments on Virgin Gorda which comprise Oil Nut Bay, Moskito Island and Rosewood Little Dix Bay Resort.

Selling predominantly to Non-Belonger investors, these developments provide a higher level of amenities than the typical development or sub-division, which is reflected in significantly higher land or property values within these developments.

Chart 5 shows the impact of these developments on property sales in the BVI where between them, sales on Oil Nut Bay, Moskito Island, and Little Dix Bay account for just 3% of all property transactions, but 33% of total sales value ($55.7M). Given that purchasers investing in these developments are predominantly Non-Belongers, this generates significant income for the Government. In round terms, Non-Belongers in these developments have contributed to 27% of total residential sales ($46M) which should have generated stamp duty in excess of $5.5M to the government.

This compares to stamp duty of $3.54M generated by sales to Belongers and $3.99M for all other Non-Belonger residential sales. Looking at the home sales of over $500,000 since 2018, this has been a market divided between the sale of damaged homes in the eighteen months or so post Hurricane Irma and the gradual return to more normalized market conditions for the past twelve months.

The impact of the pandemic on tourism and development.

At the end of 2019, the BVI tourism industry was looking forward to its first high season following Hurricane Irma where the BVI felt like a destination that had moved beyond recovery. With a growing number of tourists and many previously closed resorts and villas opened for business, including Little Dix Bay on Virgin Gorda, there was much optimism for increased tourism on land and sea alike. The number of overnight tourists had increased to 302,449 by December 2019 and was expected to grow significantly in 2020. The yacht charter industry, which had rebounded so well after Irma and supported the tourism industry in the first year, was particularly well placed to move back to pre-Irma levels of business. The Impact of the Pandemic on tourism and Development Chart 1 shows the moving average of a cruise ship and overnight (land-based and charter yacht) visitors to the BVI since 2016. The impact of Hurricane Irma in September 2017 led to a substantial reduction in visitors followed by a gradual upward trend marking the recovery. If there is a positive, it was that the lockdown in the BVI occurred near the end of the high season in late March, allowing resorts, villas, and charter companies to operate for the better part of the high season. With tourists not permitted to arrive in the BVI since March, there has been a small, but active, internal tourist market which picked up particularly in July and August as many residents chose to staycation around the BVI.In some respects, the impact of Hurricane Irma and the subsequent need to rebuild has lessened some of the impact on the BVI from the pandemic as many resorts which would have been operating are still closed or rebuilding. This includes Long Bay Beach Resort, Peter Island, Biras Creek Resort, Bitter End Yacht Club, and Saba Rock. However, for other resorts, the loss of tourism has been substantial, resulting in staff layoffs and continued uncertainty. The North Sound area of Virgin Gorda, home to many of the BVI’s leading resorts and developments, is in the process of rejuvenation, as work on Bitter End Yacht Club commenced in the summer of 2020 and with Saba Rock Resort due to reopen in April 2021. These two developments will help drive tourism back to North Sound providing much-needed amenities and facilities to visiting yachts and tourists. Having been devastated by Hurricane Irma in 2017, the owners of Bitter End Yacht Club, who have been involved in the property since the 1970s, demolished the remaining structures and reimagined what the property could become. After nearly three years of planning, the renaissance of BEYC is gaining momentum with the construction of phase one comprising the nautical village. With thirteen timber structures under various stages of construction, the village will comprise a two-story yacht club lounge complemented by upgraded docks together with The Clubhouse, comprising a multi-concept seaside restaurant and beach bar. The Bitter End Market and Reeftique will provide extensive provisioning for visiting sailors and a retail outlet for BEYC’s branded goods. With a preliminary opening date of March 2021 for this first phase, the owners are drawing on local consultants, contractors, and suppliers to help them achieve this goal in an environmentally sustainable manner which includes the upcycling of materials salvaged from the aftermath of Irma.

Situated adjacent to Bitter End, Saba Rock Resort is close to completing a multi-million dollar rebuild with plans to reopen by April 2021. Surrounded by water, Saba Rock provides visiting tourists with a unique experience of a resort, bar, and restaurant on a small island at the heart of North Sound. Learning from the devastating impacts of Hurricane Irma, the rebuilt property has benefitted from engineering suitable to withstand a major hurricane, despite the proximity to the sea. Much of the success of the North Sound area prior to Irma was due to two major developments at Oil Nut Bay and Moskito Island which together have contributed millions of dollars to the economy in direct taxes (stamp duty, payroll, and customs duties) and employment, particularly in the construction sector. At a time when the rest of the Caribbean was reeling from the economic downturn following the 2008 financial crisis, North Sound emerged as a leading tourist destination, with both developments setting new design and development standards in the BVI and regionally. With over $500M of owner investment into Oil Nut Bay Resort to date, this residential resort development has provided much-needed employment to Virgin Gorda and the BVI for more than the last ten years.

Oil Nut Bay is now a leading regional resort with all the major infrastructure components completed. Forty villas have already been completed and a further fifteen homes are under construction with a contract value of approximately $80M. The guest areas in the main resort now include the Pavilion exclusive area for in-house guests with a hot tub, fire pit, and an Asian fusion restaurant. In 2019, the marina village opened with Nova Restaurant, and at the end of that year, work commenced on the Marina Villas with three already sold plus one pre-sale with construction due to commence on the remainder of the villas. The expansion of the marina village facilities is also about to commence, adding a day spa and water sports center on the nearby beach. It is a testament to the success of Oil Nut Bay that it has managed to achieve over $20M in sales since the start of the pandemic in March. At the western entrance to North Sound lies Moskito Island which is now home to some of the most exclusive villas in the Caribbean. Developed as a private island residential retreat, this sub-division of ten sites, complete with resort areas for the exclusive use of villa owners, has set the bar for exclusive Caribbean living.

Following completion of the Branson Estate in 2015, two further villas completed construction in 2019 and were handed over to owners with a further three to have completed at the end of 2020. Construction should also break ground on one more site prior to the end of the year. Moskito Island has provided substantial employment to the construction industry during the construction phase and with three more sites still to be built out, these jobs will be secured for a number of years. The development is now ramping up the operational side as owners and guests start to enjoy the common facilities, providing additional jobs at a time when the pandemic has impacted many other businesses. In July 2020, the BVI Government signed a development agreement with the owners of Biras Creek to rebuild the hotel that was closed in 2016 and damaged by Hurricane Irma a year later. Biras sits at the head of North Sound and for many years was one of the BVI’s leading resorts. The owners are now looking to rebuild the resort with plans to complete the construction of nine new hotel rooms and a marina, which will include an 80-meter super yacht dock, together with guest facilities which will include a restaurant and beach club, retail outlets, and a provisioning store. The owners plan to have the resort operational by November 2021.

After nearly four years of rebuilding (including repair after Irma), the fully refurbished Rosewood Little Dix Bay Resort opened at the start of January 2020 with a reduced, but upgraded, room inventory of 80 units spread across a range of guestrooms, suites and villas. The resort now offers four different dining options with the addition of the new signature restaurant “Reef House” which sources locally farmed ingredients, in addition to the iconic Pavilion restaurant plus the Sugar Mill and the Rum Room. For health and well-being, the picturesque cliff-top spa has been completely refurbished, a new fitness center has been added and the six tennis courts have been rebuilt. The resort was able to operate for ten weeks before having to close its doors on 24 March, although guest reaction to the changes was extremely positive. Rosewood Little Dix Bay has retained a significant number of its employees for the duration of the closure to date, recognizing that it will have to ramp up operations extremely quickly once borders reopen, a feat that would be difficult if staff had to be rehired and trained. The period of closure has allowed the resort to prepare for a new way of operating, for the safety of guests and employees alike being a high priority. Some of the trends Rosewood Little Dix Bay is anticipating are longer guest stays and the requirement for larger accommodations. Interest in the residential units has increased as a result of the pandemic which has led to new villa construction and changes in villa ownership. Elsewhere in the BVI, Trellis Bay has seen the welcome addition of a new bar and restaurant with the opening of the Loose Mongoose, a complete redevelopment of the old beach bar and restaurant. With a thatched roof and open plan dining and bar area extending along the beach, there is also a boutique, coffee shop, and rum bar plus two substantial docks. The Loose Mongoose acts as a base for many of the outer island resorts that require docking space in Trellis Bay and an area for guests to relax before catching a boat to the outer islands.

Nanny Cay Resort and Marina has continued to upgrade the property, opening a new access road to avoid traffic passing through the boat yard. While the pandemic has impacted many of the tourist-related businesses operating at Nanny Cay, the owners have continued with the redevelopment of the hotel block which they expect will reopen in May 2021 which will complete over $10M in investment in the resort in recent years. Future plans include improvements to the boatyard, including refurbishment of some of the buildings to increase the level of service for the operation as a whole. Plans for the redevelopment of Long Bay Beach Resort on Tortola have been scaled back due to the restrictions on travel and construction, resulting from the pandemic. Demolition of the old hotel rooms commenced in July 2020.

The first phase will include the renovation of the twenty remaining beachfront rooms and the 1748 restaurant and bar, which is now open. Further development will depend on the scheduled reopening of the BVI to tourists and the lifting of travel restrictions. Scrub Island Resort, Spa, and Marina has used the closure of the BVI to tourism to enhance its guest experience program in preparation for its planned reopening. Scrub Island has also completed the construction of two new villas, the four-bedroom Drake House and the largest villa on the island, the six-bedroom Spinnaker House. Like many of the resorts with real estate programs, Scrub Island has continued to experience interest in its real estate product, resulting in a contract on one of the marina condominium units and also interest in the larger residential lots on the island. For the resort, future bookings indicate pent-up demand, as tourists seek low-density destinations and resorts that are capable of safely delivering socially distanced vacations. This demand has been boosted by the August publication of the Sports Illustrated 2020 edition which was hosted on Scrub Island in January 2020.

BVI Real Estate Market Overview

Considering the disruptions to the real estate market experienced in 2017 with Hurricane Irma and again in 2020 with the pandemic, the BVI real estate market has so far shown itself to be remarkably resilient. After the 2008 recession, the BVI property market struggled to gain momentum for a number of years with limited external investment resulting in typically twenty villa sales a year over $500,000 in value. Most of the villa sales were under $1.0M and few villas sold in excess of $3.0M. As the number of external investors reduced, the market started to see a higher percentage of Belongers acquiring villas as vendors became more willing to negotiate at lower prices. All that changed at the end of 2017 when Hurricane Irma destroyed or severely damaged much of the housing stock in the BVI. Far from reducing property sales, the damage caused by Irma created opportunities for mainly locally based investors, who were able to acquire damaged property from vendors motivated to exit. This led to an increase in the number of home sales, albeit at generally lower values reflecting the damaged nature of the properties being sold.At the same time, the market for land continued to grow as local investors bought into newly created sub-divisions mainly situated on Tortola. While there were positive signs that overseas investment in the BVI property market was picking up towards the end of 2019 and the early part of 2020, the closure of the BVI borders in March to tourists, prevented overseas purchasers from visiting the British Virgin Islands to view the property. Despite that, the isolated nature of the Caribbean Islands has appealed to the sense of security that many investors are seeking, and international inquiries for property in the BVI have remained strong. C BVI real estate market overview Reviewing the property market between 2018 and 2020 (to September), the patterns of investment that emerge, demonstrate both the activity within the local (Belonger) market and the importance of overseas investment to the real estate market as a whole and including the significant stamp duty that it generates for the Government.

The decision by Government to suspend stamp duty payments for Belongers purchasing property until May 2021 and the National Bank offering 100% financing to Belongers acquiring land has also added impetus to property transactions within the local market.

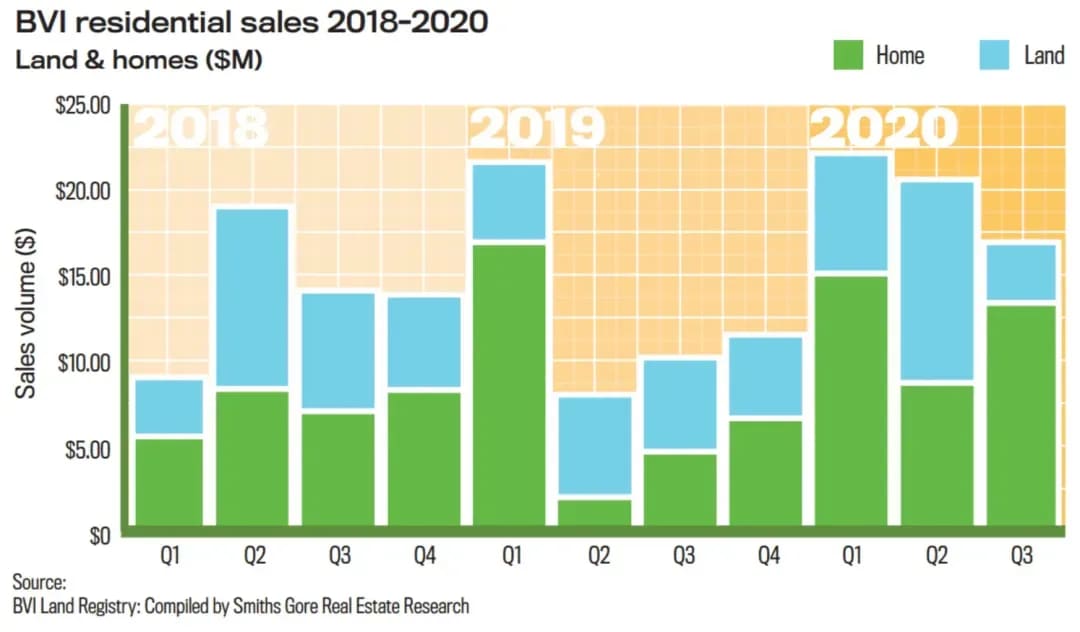

Chart 2 compiles the data for all residential property transactions in the BVI between 2018 and September 2020, divided between land and houses. In total, there was $168M of residential property sold with houses accounting for $98M (58%) and land for $70M (42%). Land sales have been evenly spread in total value between 2018 and 2020 ranging between $26.5M total value in 2018 to $20.75M in 2019. There have been $22.46M in land sales through September 2020.

The total value of house sales has increased by 26% between 2018 ($29.79M) and 2020 ($37.42M to September). House sales in 2019 totaled $30.95M

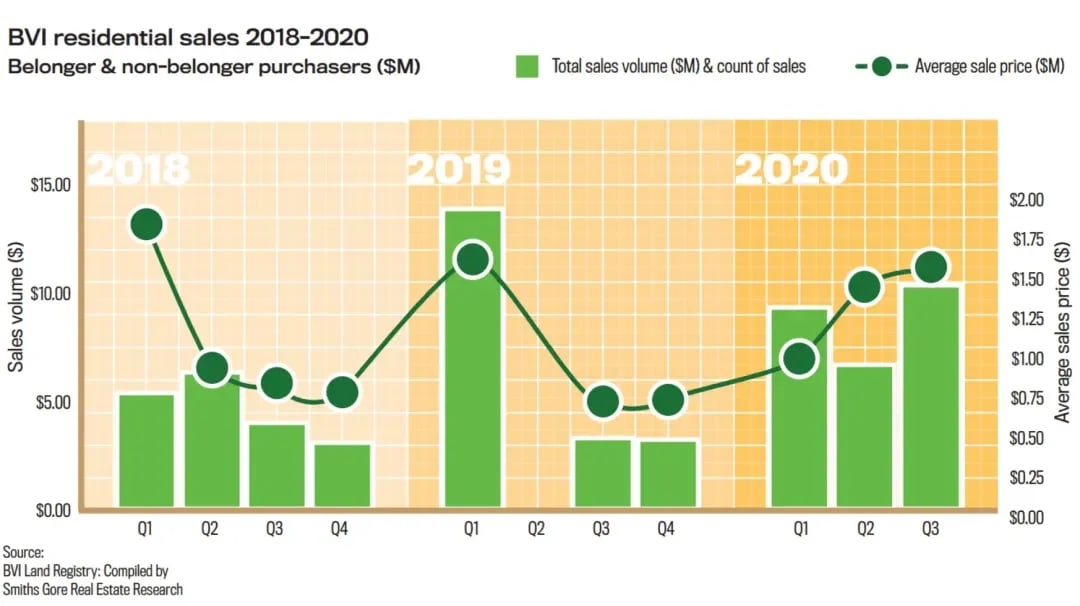

Chart 6 summarises home sales since 2018 with a total of sixty homes being sold up to September 2020. The average sale value of homes generally fell through 2018, reflecting the sale of damaged homes at lower values. Although the average price spiked in Q1 2019 due to a single home sale at $7.125M, the trend from Q3 2019 to Q3 2020 has shown a rising average house price as the residential home market moved away from the sale of damaged homes and back to more normal trading conditions of undamaged or repaired homes. In terms of total sales volume ($M), there has been a steady increase in the volume of transactions over the period with total sales of $18.81M in 2018 through 19 sales, $20.69M in 2019 (including a single home sold for $7.125M at Oil Nut Bay) through 19 sales and $26.54M to September 2020 through 22 sales. Again, this upwards trend in total sales volume reflects the changing market as the sale of damaged homes was replaced by the sale of mainly undamaged homes by late 2019 and 2020.

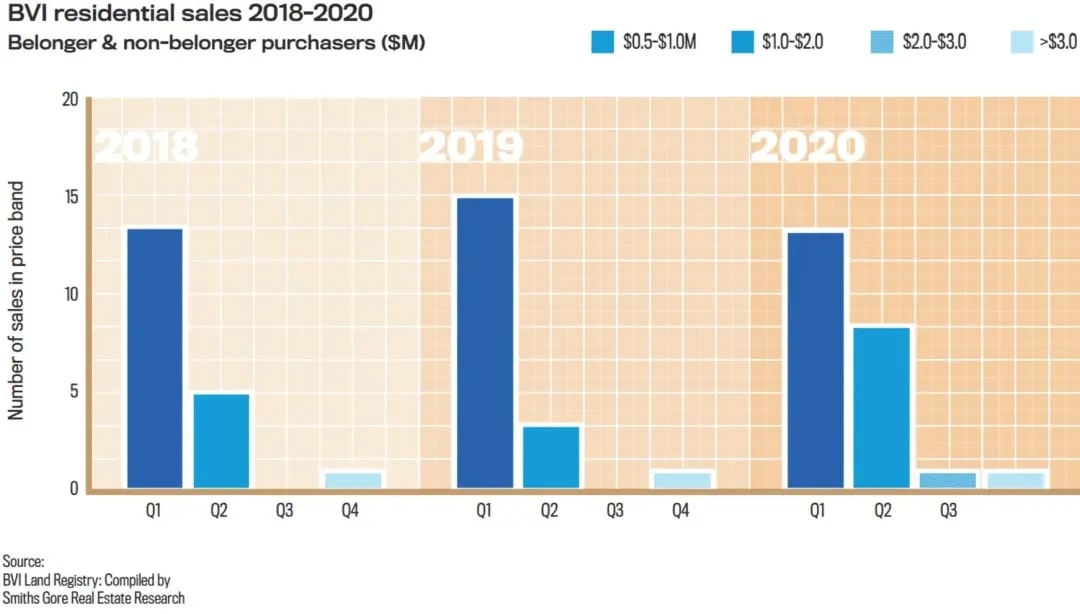

Chart 7 shows the breakdown of the sixty home sales by price band by year. This graph illustrates the same trend, with the market in 2018 dominated by home sales between $500,000 and $1.0M, only five home sales in the price band between $1.0M and $2.0M, and one sale above $3.0M. A similar pattern was evident in 2019, and again there was a single sale of a home in the $3.0M+ price range. However, by 2020, there has been a spread of home sales between the price bands, with 7 home sales between $1.0M and $2.0M and one each between $2M to $3M and over $3M.

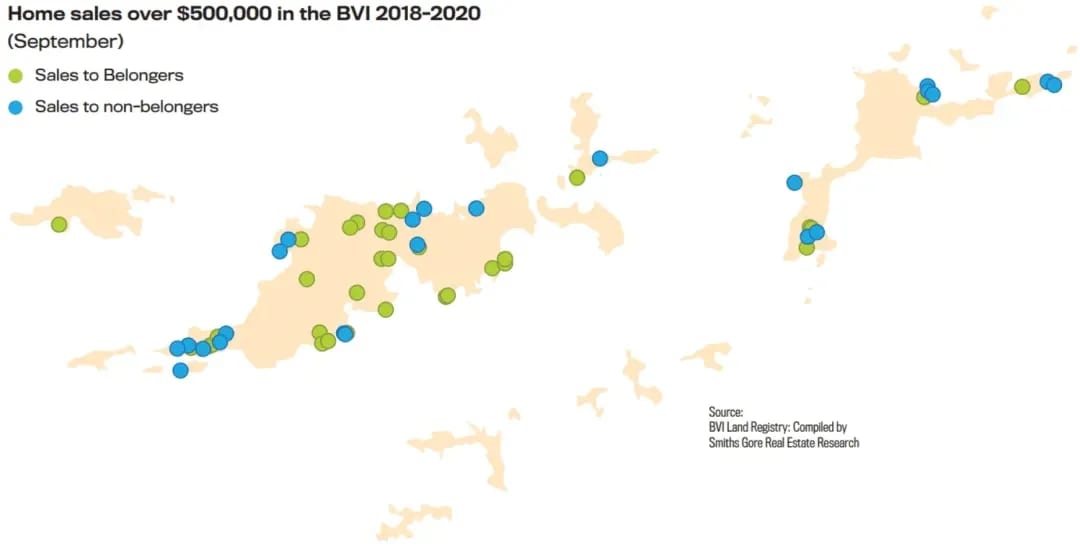

Map 3 shows the geographic spread of the sixty home sales over $500,000 between 2018 and September 2020 divided between sales to Belongers and Non-Belongers. The majority of the sales have occurred on Tortola followed by Virgin Gorda.

There have also been villa sales on Great Camanoe, Scrub Island and Jost Van Dyke. 2020 for most people has been a turbulent year, dominated by a pandemic virus which has caught politicians and scientists by surprise, leaving governments treading a fine line between re-opening the economy and trying to bring the second wave of infection back under control. There remains much uncertainty for the short term, vaccines are now just being administered. The main diversion to the pandemic was the US presidential election which was conducted alongside a resurgence of the Black Lives Matters movement and protests in the States between left and right-wing ideologies. Source: BVI Land Registry: Compiled by Smiths Gore Real Estate Research Just as with other countries, the BVI is having to grapple with the same issue of opening the Territory to tourism and the measures needed to be in place to protect the population.

The politicians, having announced their protocols to the local population and visitors alike, have had to simplify those protocols for persons wishing to visit, in light of many cancelled bookings since the protocols were first announced. Time is not on the Government’s side with what has been a very limited booking through the Terrance B. Lettsome Airport and the opening of the more travelled seaports pushed back yet again, now to 15 April 2021.

With the winter season now almost behind us, uncertainty remains for many tourist-related businesses. While the real estate market has proven to be remarkably resilient post-Hurricane Irma, a healthy economy is an essential part of the success of the real estate market. The next six months will be critical to the future of the BVI.

The UK’s position has been complicated as a result of the November 3 election in the United States, where the change in administration in January 2021 heralded a new president with sharply different policies and Irish roots, who has already stated that any threat to the Good Friday agreement will impact the UK’s ability to reach a trade agreement with the USA. The November election, which saw the election of Joe Biden, was the culmination of four years of the Trump Administration, following the other electoral surprise of 2016 when Donald Trump emerged victorious against then-favorite, Hilary Clinton.

The fact that President Trump never conceded the election to President Joe Biden, serves as a postscript to an unorthodox presidency, where fake news and firing by Twitter became as much a part of the White House as foreign and domestic policy. The fact that over 70 million Americans voted for President Trump in 2020 reflects the huge appeal he still has to his base and the continued importance that he has in setting the agenda for the Republican party going forward. While controlling both the House of Representatives and Senate is political Nirvanah for any president, allowing them to push through their agenda with little opposition, the markets generally prefer the L Checks and balances – US election postscript “stability” of a divided Congress, where a break can be applied to any president looking to push an agenda considered too radical for mainstream politics. Each of the last four presidents was elected with majorities in both House and Senate, but lost control of one chamber at the mid-term elections, preventing them from effectively continuing their agendas and pushing the Government towards gridlock.

The checks and balances set up by the Founding Fathers have practical consequences well beyond those they first envisaged. The markets continue to rally since the election, boosted by news of three COVID-19 vaccines that have been shown in testing to be effective against the virus. While it will still take time for vaccination programs to be fully implemented, an end game could be in sight, even if it is still months away. Confidence in the stock market, combined with continued low interest rates, will have a corresponding knock on real estate investment, which has already demonstrated real growth despite the pandemic setbacks.

The US economy is not out of the woods though, with Biden and the Democratic Leadership in both Houses of Congress having decided to use the budget reconciliation process to pass what is currently a $1.9 trillion COVID relief bill, which has strong bipartisan support among the public. There is light at the end of the tunnel for the economic downturn driven by the pandemic. With the Biden administration well into its second month in office, the near-term outlook for the BVI remains positive on two fronts.

First, the recent announcements regarding vaccines will enable the Government of the BVI and businesses to work towards normalcy with a more definitive timetable of six to nine months. Second, there is hope that economic growth will continue as confidence deepens and markets remain buoyant. Positive economic growth in the US normally promotes similar confidence in the Caribbean.

Chart 6 summarises home sales since 2018 with a total of sixty homes being sold up to September 2020. The average sale value of homes generally fell through 2018, reflecting the sale of damaged homes at lower values. Although the average price spiked in Q1 2019 due to a single home sale at $7.125M, the trend from Q3 2019 to Q3 2020 has shown a rising average house price as the residential home market moved away from the sale of damaged homes and back to more normal trading conditions of undamaged or repaired homes. In terms of total sales volume ($M), there has been a steady increase in the volume of transactions over the period with total sales of $18.81M in 2018 through 19 sales, $20.69M in 2019 (including a single home sold for $7.125M at Oil Nut Bay) through 19 sales and $26.54M to September 2020 through 22 sales. Again, this upwards trend in total sales volume reflects the changing market as the sale of damaged homes was replaced by the sale of mainly undamaged homes by late 2019 and 2020.

Chart 7 shows the breakdown of the sixty home sales by price band by year. This graph illustrates the same trend, with the market in 2018 dominated by home sales between $500,000 and $1.0M, only five home sales in the price band between $1.0M and $2.0M, and one sale above $3.0M. A similar pattern was evident in 2019, and again there was a single sale of a home in the $3.0M+ price range. However, by 2020, there has been a spread of home sales between the price bands, with 7 home sales between $1.0M and $2.0M and one each between $2M to $3M and over $3M.

Map 3 shows the geographic spread of the sixty home sales over $500,000 between 2018 and September 2020 divided between sales to Belongers and Non-Belongers. The majority of the sales have occurred on Tortola followed by Virgin Gorda.

There have also been villa sales on Great Camanoe, Scrub Island and Jost Van Dyke. 2020 for most people has been a turbulent year, dominated by a pandemic virus which has caught politicians and scientists by surprise, leaving governments treading a fine line between re-opening the economy and trying to bring the second wave of infection back under control. There remains much uncertainty for the short term, vaccines are now just being administered. The main diversion to the pandemic was the US presidential election which was conducted alongside a resurgence of the Black Lives Matters movement and protests in the States between left and right-wing ideologies. Source: BVI Land Registry: Compiled by Smiths Gore Real Estate Research Just as with other countries, the BVI is having to grapple with the same issue of opening the Territory to tourism and the measures needed to be in place to protect the population.

The politicians, having announced their protocols to the local population and visitors alike, have had to simplify those protocols for persons wishing to visit, in light of many cancelled bookings since the protocols were first announced. Time is not on the Government’s side with what has been a very limited booking through the Terrance B. Lettsome Airport and the opening of the more travelled seaports pushed back yet again, now to 15 April 2021.

With the winter season now almost behind us, uncertainty remains for many tourist-related businesses. While the real estate market has proven to be remarkably resilient post-Hurricane Irma, a healthy economy is an essential part of the success of the real estate market. The next six months will be critical to the future of the BVI.

Checks and balances – US election postscript

Looking back, 2016 was an auspicious year for voting, with both Brexit and the US presidential election ending in surprise results. The Brexit referendum in June of that year returned a slim majority in favor of leaving the EU, resulting in four tumultuous years for the UK (and by extension Europe) as politicians and the public grappled with the complexities of exiting their uneasy relationship with their European neighbors. As 2020 drew to a close, the final hurdles of negotiating a trade deal with the EU remained to be crossed, but with a ‘no deal exit seemingly less of a threat. With both the UK and Europe facing a serious COVID-19 second wave and being forced into regional and national lockdowns, it seems as if the negotiations will go down to the wire before an acceptable compromise is reached.The UK’s position has been complicated as a result of the November 3 election in the United States, where the change in administration in January 2021 heralded a new president with sharply different policies and Irish roots, who has already stated that any threat to the Good Friday agreement will impact the UK’s ability to reach a trade agreement with the USA. The November election, which saw the election of Joe Biden, was the culmination of four years of the Trump Administration, following the other electoral surprise of 2016 when Donald Trump emerged victorious against then-favorite, Hilary Clinton.

The fact that President Trump never conceded the election to President Joe Biden, serves as a postscript to an unorthodox presidency, where fake news and firing by Twitter became as much a part of the White House as foreign and domestic policy. The fact that over 70 million Americans voted for President Trump in 2020 reflects the huge appeal he still has to his base and the continued importance that he has in setting the agenda for the Republican party going forward. While controlling both the House of Representatives and Senate is political Nirvanah for any president, allowing them to push through their agenda with little opposition, the markets generally prefer the L Checks and balances – US election postscript “stability” of a divided Congress, where a break can be applied to any president looking to push an agenda considered too radical for mainstream politics. Each of the last four presidents was elected with majorities in both House and Senate, but lost control of one chamber at the mid-term elections, preventing them from effectively continuing their agendas and pushing the Government towards gridlock.

The checks and balances set up by the Founding Fathers have practical consequences well beyond those they first envisaged. The markets continue to rally since the election, boosted by news of three COVID-19 vaccines that have been shown in testing to be effective against the virus. While it will still take time for vaccination programs to be fully implemented, an end game could be in sight, even if it is still months away. Confidence in the stock market, combined with continued low interest rates, will have a corresponding knock on real estate investment, which has already demonstrated real growth despite the pandemic setbacks.

The US economy is not out of the woods though, with Biden and the Democratic Leadership in both Houses of Congress having decided to use the budget reconciliation process to pass what is currently a $1.9 trillion COVID relief bill, which has strong bipartisan support among the public. There is light at the end of the tunnel for the economic downturn driven by the pandemic. With the Biden administration well into its second month in office, the near-term outlook for the BVI remains positive on two fronts.

First, the recent announcements regarding vaccines will enable the Government of the BVI and businesses to work towards normalcy with a more definitive timetable of six to nine months. Second, there is hope that economic growth will continue as confidence deepens and markets remain buoyant. Positive economic growth in the US normally promotes similar confidence in the Caribbean.

While significant short-term concerns remain for the tourism industry, definitely, there is hope on the horizon. Roll on 2021.